Home Owners Insurance Claims

Home Owners Insurance Terms

A Little Advice

Beware of any contractor who:

- Provides you with an inaccurate invoice to give your insurance company. On a recoverable depreciation policy, you or your contractor could unknowingly commit fraud by representing to your insurance company that the cost of repairs was higher than the actual final cost.

- Claims they can cover your deductible. In order to replace your roof for so little, the contractor would need to severely cut corners that would result in poor quality work.

- Offers to give you money back after you pay them the entire claim amount. This is a common strategy used by fly by night roofers and storm chasers to take advantage of homeowners.

We can assure you, it is cheaper in the long run to hire a reputable company and have the work done right the first time. If you hire the cheapest contractor and pay with an insurance claim, you could end up hiring a second contractor to repair the shoddy work and that work will be 100% out of pocket.

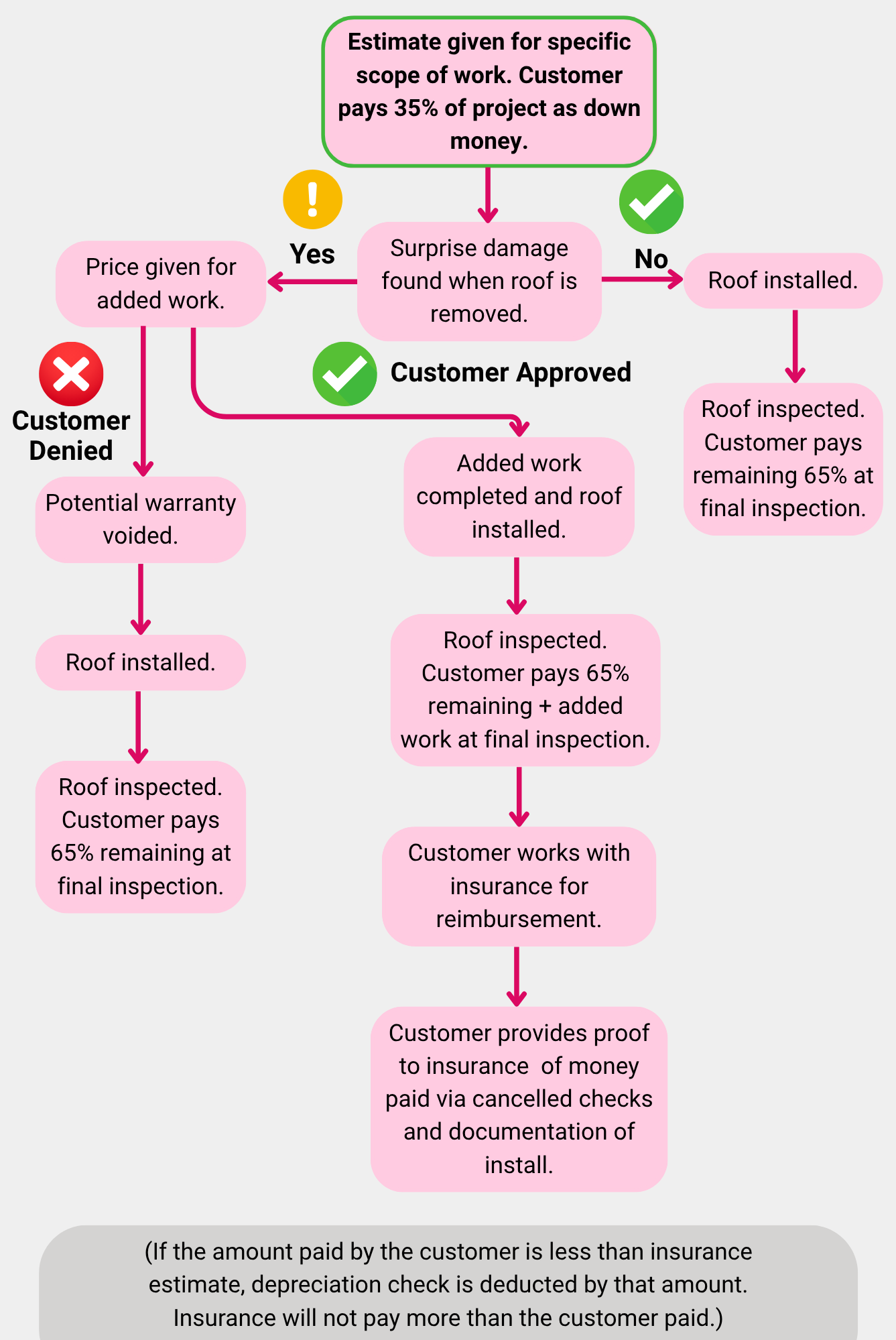

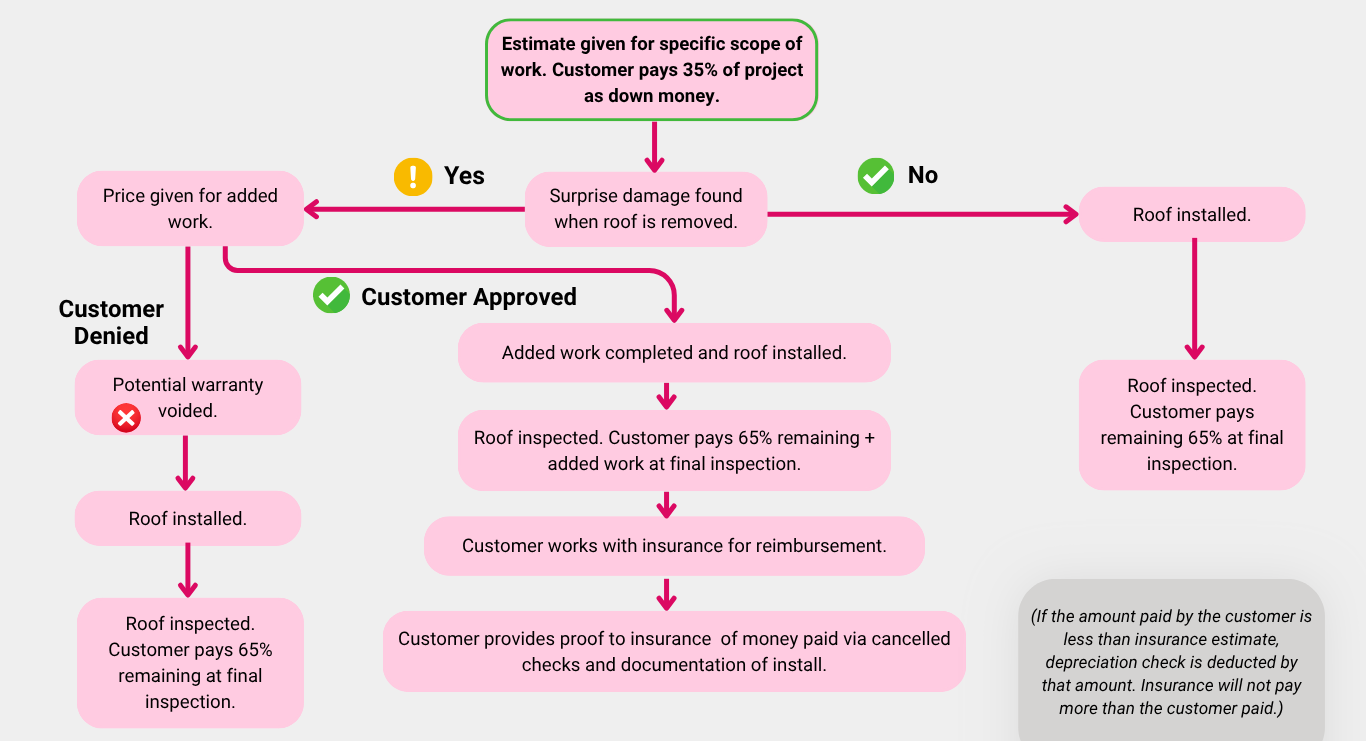

Understanding the Insurance Process

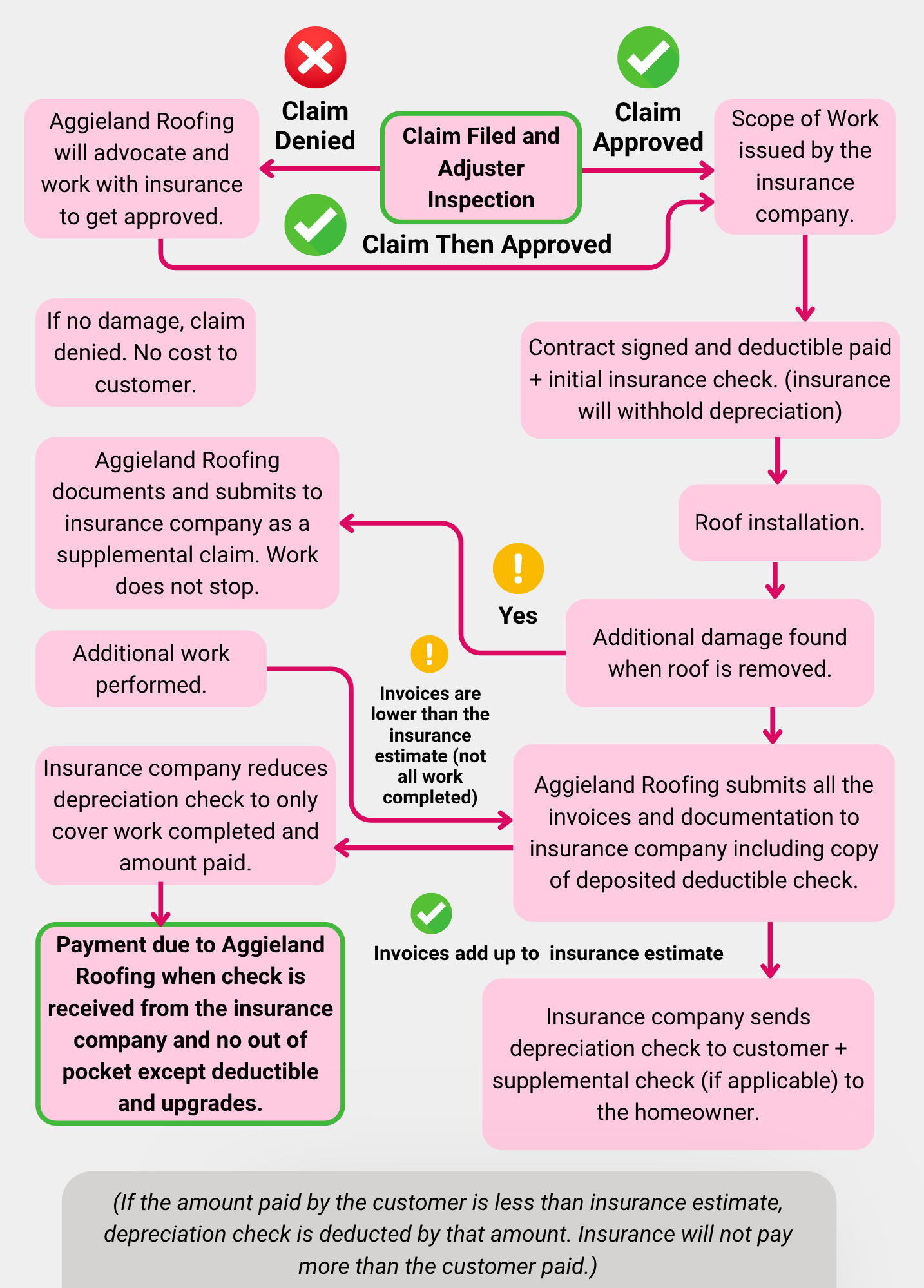

① INSURANCE CLAIM

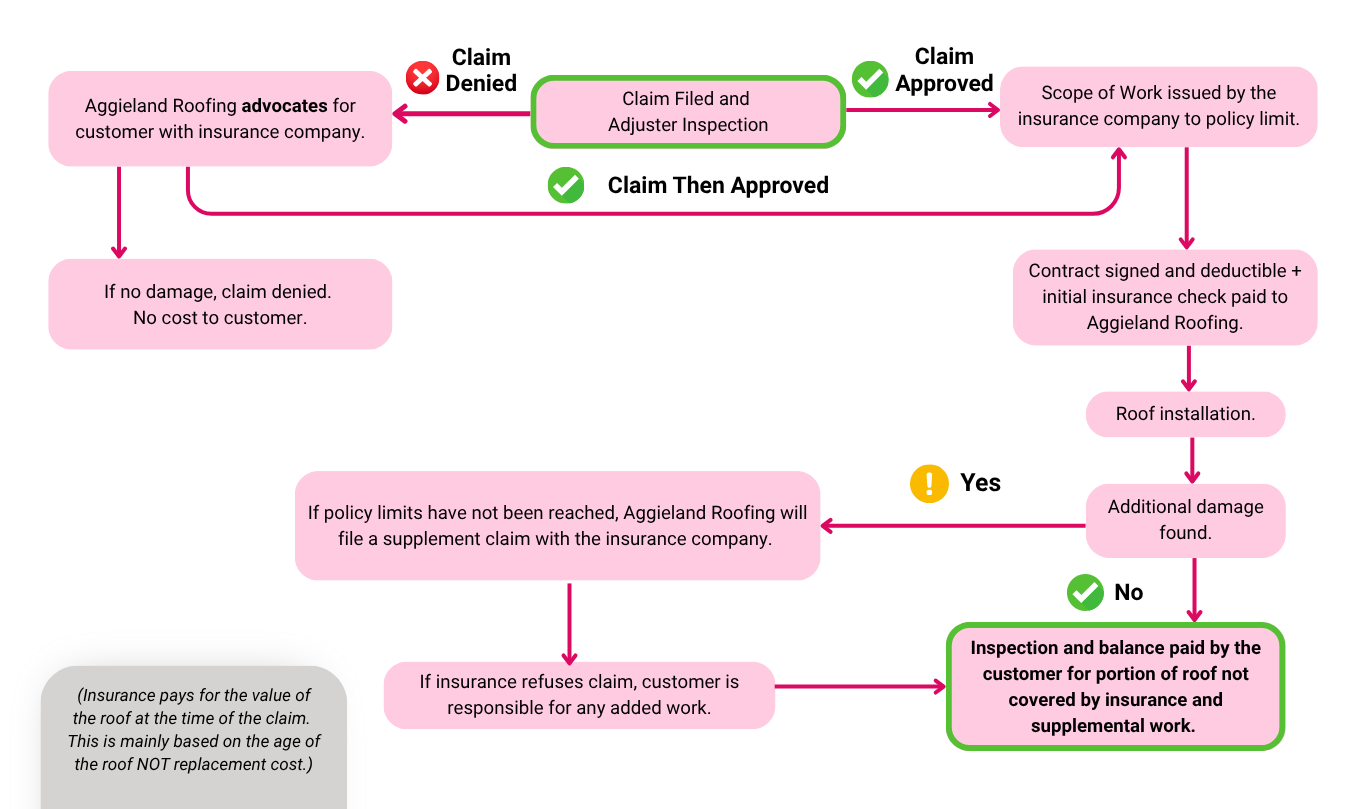

② ACTUAL CASH VALUE (ACV) INSURANCE CLAIM

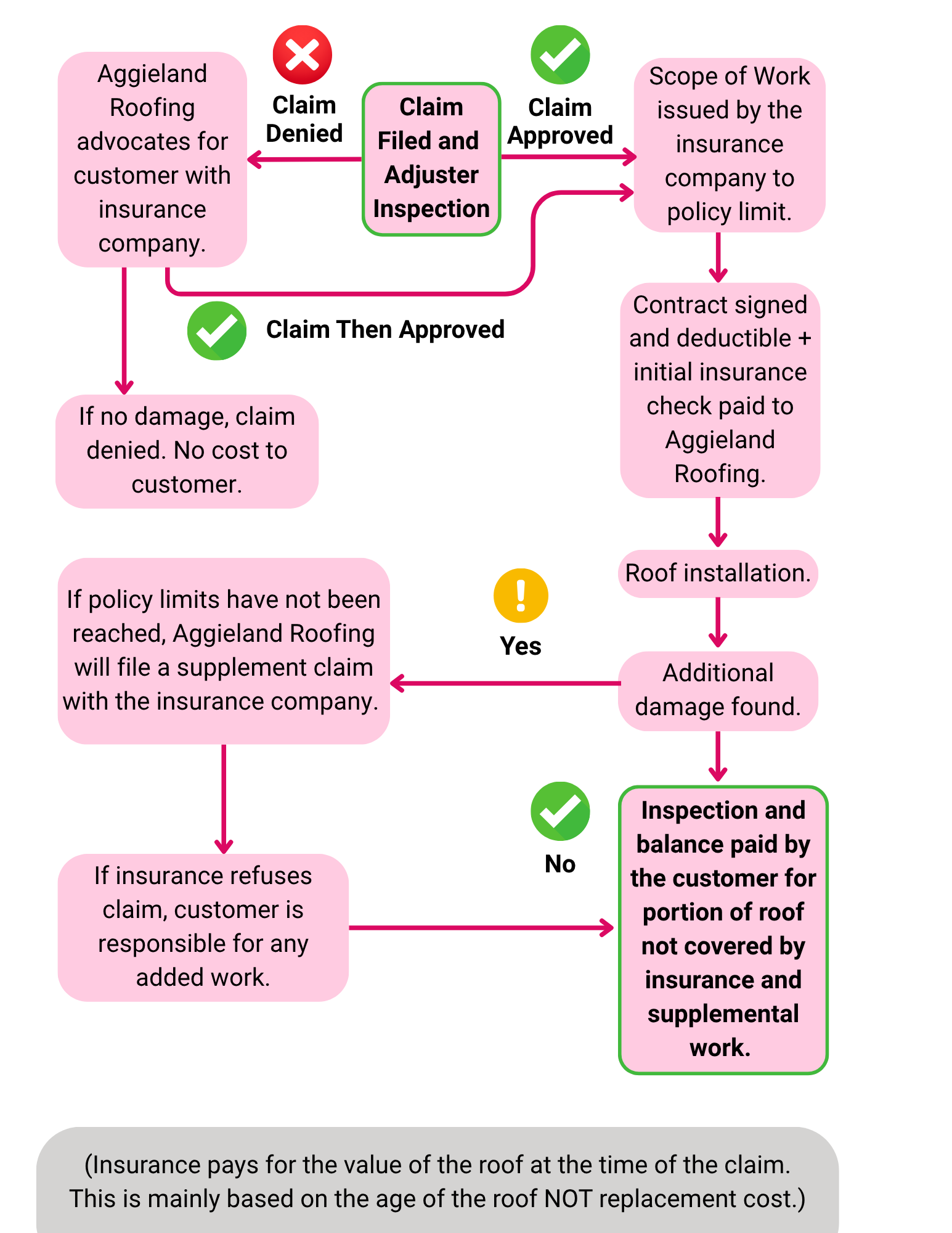

② CASH JOB

SPEAK WITH A ROOFING SPECIALIST TODAY!

Contact us today to speak with an experienced roofing specialist and to schedule a free estimate!